Avalara - Creating a global compliance platform

There are only two certainties in life; death and taxes. Avalara is working towards its ambition of being the key tax partner for businesses and governments around the globe to handle the complexity.

Avalara (ticker: AVLR) is an American software company founded by Scott McFarlane. The company provides businesses with cloud-based automated tax software. Founded in 2004, the company has built a compliance platform to help businesses navigate the complexity of taxes. The company sells its product through partner referrals and direct sales to businesses.

Why is Avalara interesting?

Avalara interests me for different reasons. First, the company solves a problem that is easily understandable. As businesses grow and sell more products & services and sell to customers across geographies, taxes get complex very quickly. Avalara promises to simplify and automate the complexity.

Second, the market is early in its adoption of automated tax solutions. Avalara's main competitor is Excel and manual tax administration. As businesses adopt the Digital Transformation trend, it seems inevitable that automated tax solutions displace manual processes.

Third, the business sits at the intersection of multiple trends that could last well beyond 2030. Digital Transformation, eCommerce, omnichannel selling, and increased regulatory requirements are the main drivers behind what will lead to businesses reconsider how they handle taxes. Avalara has the opportunity to address these needs and add products to its platform.

Finally, if Avalara executes on its ambitions, the company could grow at high rates for the foreseeable future and I would hope to see operating leverage to translate this into Free Cash Flow.

Business

Avalara's platform is called the Avalara Compliance Cloud. The platform offers tax calculations (AvaTax), returns (Avalara Returns), compliance document management, licensing, registration, and tax content. Avalara sells its products as a Subscription-as-a-Service (Saas) model and usage-based pricing (based on the number of calculations, filings, etc.).

The Compliance Cloud helps businesses automate the process of tax calculations, filings, etc. to the jurisdiction that requires this. The US Supreme Court decision in the South Dakota v. Wayfair case in 2018 was that states may charge taxes on transactions even if the seller has no physical presence in the state. This essentially means California can charge tax on a transaction if the buyer is located there, but the seller isn't. This ruling has led many businesses to reconsider how they approach the calculation and administration of sales tax and the government to start collecting these taxes. Without a way to track all this, businesses expose themselves to tax liabilities or even penalties as governments start enforcing the tax rules. Avalara provides an automated solution for the cost of less than one full-time employee that reduces the amount of work needed to administer this and potential liabilities.

To give an idea of the complexity of selling online can be, consider that there are 11000 tax jurisdictions in the US alone and that each has its own tax rates, rules, and filing requirements. The complexity grows exponentially as a business wants to sell across sales channels or even national borders.

The Avalara Compliance Cloud has a database of tax content (jurisdiction boundaries, product classifications, tax rates, and other tax rules). Through an API (Application Programming Interface), the Avalara Compliance Cloud integrates with customer systems and its partner ecosystem. Avalara's partner ecosystem is cited as one of its primary competitive advantages. With over 1200 partner integrations, Avalara is pre-built into Customer Relationship Management (CRM), Enterprise Resource Planning (ERP), Point-of-Sales (POS) systems, marketplaces, and eCommerce applications (Shopify, Magento, BigCommerce, Wix). Because the Compliance Cloud is cloud-based, the database is constantly updated and client requests receive the most up-to-date information. This enables accurate real-time calculations of taxes.

These integrations with business applications also facilitate the aggregation of data from all these different sources. For example, a merchant who sells online as well as in a physical store might use Stripe to sell on his website which is done through a Wix website, and use Lightspeed to sell in-store. He could also use Salesforce as a CRM, Xero’s accounting software, and SAP as an ERP. To accurately calculate and file taxes for every transaction, this merchant needs a solution that has integration with all these providers. The amount of relationships and integration Avalara has is very hard to replicate and is central to the customer's purchasing decision because of how it impacts ease of use.

Source: Analyst Day 2022

With businesses being less and less limited by their physical location to make sales and sell through multiple channels (omnichannel), this presents a tax compliance problem. Merchants selling through eCommerce platforms like Shopify, BigCommerce, and Wix can use pre-built applications from Avalara and other vendors or can choose to directly purchase software solutions from a vendor. Marketplaces like SeatGeek, Vivino, Wish and Coursera directly use the Avalara Compliance Cloud to comply as the burden to comply with tax regulation is mostly put on the marketplace operator. Large online businesses like Amazon have often built their own internal solution to this problem, but the amount of resources needed to maintain such a system is too demanding for most businesses.

It would be a mistake to label Avalara as just a sales tax calculation and returns software. Sales tax was just the problem businesses most commonly encountered and the first step to expand its product suite. Through acquisitions, Avalara has acquired product capabilities across a range of compliance-related subjects:

"Since 2018, we have acquired beverage alcohol tax, cross-border transaction (e.g., tariffs and duties) solutions, business licenses, insurance tax compliance solutions, and artificial intelligence technology and expertise." - Annual Report 10-K 2021

For example, Avalara is determined to capture the European market by offering e-invoicing solutions in addition to VAT, duties, and tariffs. For its cross-border product, Avalara automatically classifies an item with the correct code to make sure it clears customs. This avoids bad experiences like items being held at customs or additional payments being required due to misclassification. This classification is done using Artificial Intelligence.

In addition to selling to businesses through pre-built integrations, directly or through marketplaces, Avalara has also launched its Managed Returns for Accountants product. This product essentially offers the benefits of the Avalara Compliance Cloud to accounting firms. Many businesses are still relying on their accountants for their tax administration. By also offering its solutions to these service providers, Avalara hopes to capture a larger percentage of potential customers.

The acquisition of TTR (Transaction Tax Resources) is key to Avalara's ambition of becoming the largest automated tax service provider. TTR has amassed a large database of tax content and has customer relationships with many large businesses that rely on its extensive database for their tax decisions. This acquisition helps Avalara compete with older, established competitors that might have had an advantage on the tax content.

Avalara's ambition go beyond the US market and its acquisition of Inposia in Germany gives it access to tax content and e-invoicing capabilities in Europe. The European Union has adopted laws that mandate suppliers to send the government e-invoices in a pre-determined format. The standards for e-invoices differ per country and some countries even have mandates for Business to Business (B2B) and Business to Consumer (B2C) invoicing. France, for example, plans to mandate e-invoicing for B2B transactions starting in 2024. Governments also can mandate companies to clear e-invoices by the tax authority before it is sent to the client. Other governments require regular reporting to the tax authority after the e-invoice is sent. As countries across Europe and other regions choose their model and require more reporting from businesses, businesses that sell in these jurisdictions must have an efficient way of handling all those different requirements.

Here again, the digitalization of invoicing and more reporting requirements by the government seem inevitable. The direction the world is going is clear, companies will have to calculate, report and remit taxes as close to real-time as possible as well as comply with digital administration mandates. Avalara sees this as an opportunity towards their goal (dream) of being a part of every transaction in the world.

These are key trends that should fuel growth for Avalara outside the US as it can bundle the Avalara Compliance Cloud and e-invoicing. This, of course, assumes businesses find additional value in bundling these functions. There are plenty of companies just offering e-invoicing. It will take some convincing from Avalara to convince the value of this bundle. To me, it seems intuitive to have the calculation, invoicing and reporting done in the same place.

Despite these clear trends, International growth seems to slow down.

Source: Analyst Day 2022

The reason for this slowdown in growth could be as simple as the incredible growth experienced in 2021. To compete in the non-US market, it seems clear from my research that Avalara will need more tax content and tailor its capabilities to the local needs. This could be very lucrative, but it will take a lot of effort and resources to capture a significant part of the market. If Avalara manages to reach this point, it could significantly further their efforts in capturing Enterprise customers that sell globally.

Market & competition

As of right now, Avalara has mostly been focused on the Mid-Market (50-500 employees) and Small and Mid-sized Businesses (SMB) segments. Their largest competitor in this segment is manual processes. It is clear that a large percentage of the businesses in this segment will transition to automated solutions eventually.

In the Enterprise market however, the competition is more fierce. Avalara has stated that they want to move upmarket and onboard more Enterprise customers. This requires a different focus for the salesforce as sales cycles are much longer and contracts much larger and complex. Vertex Inc, Thomson Reuters and Wolters Kluwer have provided tax services to these very large businesses. All these competitors also have relationships with multinationals outside the US and displacing the relationships with Enterprises seems much more complicated.

Vertex, for example, boasts more than 4200 customers and >50% of the Fortune 500 is a Vertex customer. Besides the direct relationships with Enterprises, Vertex specifically mentions its relationships with the largest tax and accounting firms (KPMG, Deloitte, Ernst&Young, etc.), pre-built integrations with major software vendors (though probably a lot less than Avalara but tailored to the Enterprise market) and, the ambition to move downmarket to compete with Avalara in the Mid-market.

Both Vertex and Avalara estimate that the TAM (Total Adressable Market) is penetrated <10%. The TAM in the US alone is estimated to be ~$8B. Outside the US the TAM is estimated around ~15B. Considering the size and penetration level of the TAM, there is room for more than one software provider for this problem that will affect businesses of all sizes. Although I understand Avalara's strategy to move upmarket, this is a strategy that seems more complicated and potentially expensive than what its competitor Vertex is doing. The early signs have been that Avalara is much more aggressive and move much faster than Vertex.

Source: Vertex investor presentation June 2022

For what it’s worth, I think there is room for both to do well but Avalara seems to have the ambition to win it all.

Customers & partners

During their recent Analyst Day, Avalara gave more details about their customer numbers. Below charts stood out to me:

Source: Analyst Day 2022

What stood out to me was how diversified Avalara's revenues are. At this point, Avalara is not overly reliant on any one market segment. Second, this confirms why Avalara wants to capture a larger part of the Enterprise market. The ARPU of $76000 comes close to Vertex's $78000 and is roughly 3x what the average SMB contributes.

Besides its customer split, Avalara is not overly reliant on any one partner (like Shopify) and has control on its pricing (~12% of revenue has some influence from partner).

Source: Analyst Day 2022

CEO Scott McFarlane always cites deals made in the quarter. The size and industry where new customers come from are incredibly varied. This is supported by the above charts and the industry split below.

Source: Analyst Day 2022

Competitive advantage

Switching costs: Once implemented and adopted by a customer, Avalara's solutions are integrated into the organization and costly to rip out. Avalara essentially has one job, to automate tax and do it well. As long as they do that well, maintain their integrations with partners and offer additional products that may be of use, there not many reasons for a customer to even consider switching. This works the other way around as well, especially in the Enterprise segment where competitors already have relationships. However, the market penetration and direction of the market make me confident there is plenty of fish left in the sea for Avalara and their competitors.

Network effects: Although I believe there are some network effects at play here, I don't want to overstate the strength of this competitive advantage in this context. We often associate network effects with businesses like Google, Meta and the payment networks. The network effect is not nearly as strong here and I was doubtful about even naming it. But it is clear the partner network does help acquire and retain customers. Avalara benefits from the largest partner network that refer customers and make it incredibly easy for businesses to be onboarded. The more partners join, the more businesses will be attracted to Avalara due to its integrations. Consequently, partners will be more likely to nurture a relationship with Avalara to service their own customers better. Additionally, Avalara invests in their AI/ML capabilities to better identify products for classification purposes. More data to improve accuracy is the name of the game here and it improves Avalara's product for all customers.

Management & Ownership

It is good to see a founder still at the helm 18 years after having founded the business. Scott McFarlane is still the CEO of the company and sounds excited to lead them into the next decade of growth. However, this enthusiasm is not reflect by his shareholdings. He currently owns approximately 0.8% of the shares outstanding, far from what I'd consider and owner operator.

There is no significant (active) shareholder to speak of. McFarlane receives ~$600.000 in annual salary and receives his long-term incentives in the form of Restricted Stock Units (RSU's, 40% of long-term incentives) and Performance Stock Units (PSU's, 60% of long-term incentives).

The performance metrics used to determine the annual cash bonus is based new and upsell bookings, Non-GAAP Gross Margin, Non-Gaap Operating Income and Customers at Risk.

The PSU's are based on Revenue CAGR during the period (includes acquisitions as long as aggregate acquired revenue is >$100M. Note that the total PSU payouts will be based on the 2021-2023 period. The 2021 target was 23%, compared to a 39% CAGR in the period. This begs the question, are these target set too low or was business performance just exceptionally good in 2021?

Although McFarlane's share ownership is not significant based on the shares outstanding, the value of the equity grants he receives on a yearly basis is multiples of the salary he makes. The same applies for CFO Ross Tennenbaum and COO Amit Mathradas. This is an incentive to create equity value, but it is still equity that is given away by diluting other shareholders. I would consider alignment between shareholders and management to be somewhat aligned at best.

Quality Score

As I explained in my latest quarterly update, I will compute the Quality Score of every company I write up to compare to other companies I have looked at. The scoring system is proprietary for now and will be refined over time, but I can reveal it attributes scores based on higher margins, organic growth, positive and growing cashflows, high returns on invested capital, management tenure, a track record of sound capital allocation and insider ownership as these are the base qualities I am looking for.

Avalara's quality score is 65

The lack of shareholdings by insiders, negative cash flows (treating SBC as cash expense), and many acquisitions worked against Avalara in the scoring. The organic growth runway, strength of the value proposition, switching costs, and growth track record worked in its favor.

Source: Own scoring

Financials & Valuation

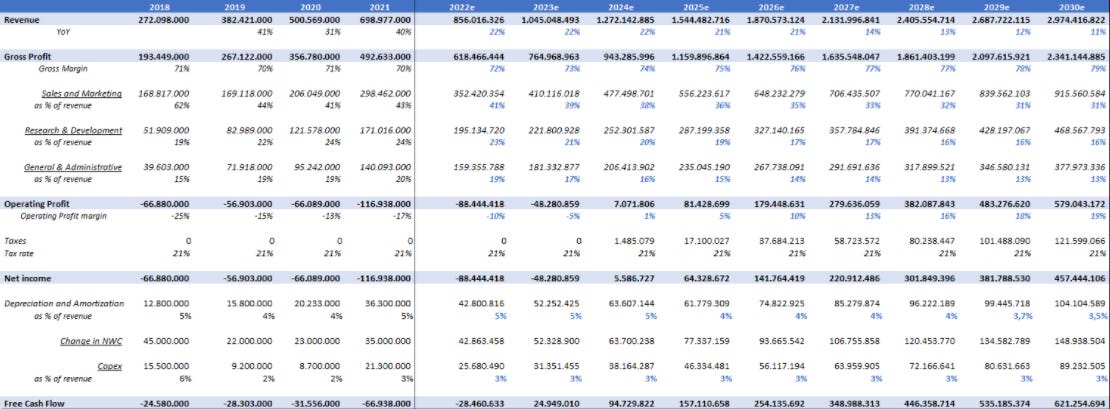

Here is an overview of Avalara's financials since 2018.

Source: SEC filings

As you can see, with ~$700M in revenue, the company still reports an operating loss. The company has grown its costs base almost as fast as its revenues, which gives me some pause. Even General and Administrative costs, which often have the most operating leverage, have increased to become a larger percentage of revenue. Now, the company might have hired and grown its cost base ahead of future growth. The push towards moving upmarket only dates back to 2020/21 and it is natural to see a lot of costs before new Enterprise customers are onboarded. After all, Enterprise customers expect more support from their vendors and sales cycles are longer.

This data point brings me to a recent rumor. Vista Equity Partners, the renowned Software-focused Private Equity firm, was rumored to be interested in taking Avalara private. We have seen Anaplan go private after Thoma Bravo offered a 30% premium to the share price not too long ago, a ~13x Forward EV/Revenue multiple for a company growing at ~30% a year and still with negative margins. Other software companies like Everbridge and Avalara have now been rumored to be targets for PE. If PE is so interested at these seemingly high multiples, how much leaner could these companies be? I think the answer for Avalara is that it could be much leaner and still grow at an acceptable rate. I am not sure if this is what management is really focused on, and I strongly suspect the people at Thoma Bravo and Vista Equity Partners are.

Now back to the financials.

The company has been able to grow its revenue per customer by maintaining a Net Revenue Retention rate above 107% for years. This gives a good baseline to grow revenue even further as the company also adds new customers at a decent pace.

Source: SEC filings

Avalara posted its medium and long-term operating model during the most recent Analyst Day. Keep in mind that these are Non-GAAP numbers, meaning they exclude Stock-based compensation. The numbers shown in the spreadsheet above are GAAP numbers and include SBC.

FY 2025 target

Source: Analyst Day 2022

Long-term operating model

Source: Analyst Day 2022

The company clearly sees a path toward Free Cash Flow margins 15-20% at maturity. I, however, am inclined to be skeptical that it will be reached within 3-5 years based on the company's history. I modelled a scenario in the event management is a bit too optimistic on these projections, but not miles off. This yields the following projections.

Source: Own estimates

Note that this scenario implies a material slowdown in the growth of costs and a steady growth in revenue in the decade ahead. Considering that Avalara has negative FCF or barely breakeven at $700M in revenues, I have trouble seeing how they can change the mentality regarding costs around this quickly.

Avalara sits at the intersection of many trends that could provide for growth in this decade and the next. Given this context management might have being doing the right thing by reinvesting every penny in the business. However, even with such an optimistic outlook, the valuation doesn't seem that compelling. Say the company would be able to hit this bold projection, more than tripling revenues, operating margins approaching 20% and ~$600M in Free Cash Flow by 2030, what would the company be worth?

Assuming a 17x multiple of FCF, Avalara would be worth just over 10B, or 20% more than today's market cap. Investors would maybe receive some cash between now and then, but considering the dilution that happens in the meantime (say 4-6% a year at the low-end), it is difficult for me to find Avalara attractive at today's prices. To be long Avalara at this valuation, an investor must have a lot of confidence in 1) the growth trajectory, 2) its duration beyond 2030 3) the operating leverage in the business and 4) management's ability to deliver the operating leverage and revenue growth rates ~20% per annum.

If someone has a different view on this than me, I'd love to hear it. I'm fond of the business and can see how it can grow to be profitable and much larger in the future, I just have trouble seeing how shareholders capture this value creation at today's market prices.

Conclusion

Avalara benefits from multiple large trends that will make its business more and more relevant. The value proposition to customers will only get better as government requirements grow and complexity compounds. The costs to the customer are relatively low compared to the efficiencies gained from automation and, perhaps even more important, the liabilities and penalties the companies avoid.

The company has done a good job to position itself as one of the leaders in this transition. Although it has some competition in the Enterprise segment, the Mid-Market and SMB segments seem ripe for the taking and are large enough to support growth for many years. Founder Scott McFarlane, who, despite not being a large shareholder, still seems very passionate about the business and has bold ambitions.

On the more negative side, I have my doubts about management's ability to deliver on the operating leverage. Some drastic changes will have to be made to the cost base for me to be convinced Avalara can be able to generate significant cash flows in the near future (say 3 to 5 years). Combine this with incentives based on Non-GAAP numbers that exclude dilution (SBC) and focused mostly on revenue growth, it does not bode well for value creation through growing FCF per share. Unfortunately for shareholders, a high FCF per share growth rate is exactly what is needed to justify the current valuation. The projections shared under Financials & Valuation already feel overly optimistic to me despite the direction the world is going clearly working out well for Avalara. Where bulls will probably disagree with me is on the duration of ~20% revenue growth and the confidence level about when operating leverage kicks in to reach the promised land of 20-25% operating margins.

Avalara still interests me. Adoption of automated tax solutions seems inevitable to me and the burden will soon become to much for most businesses to bear. They will need someone like Avalara and there is reason to believe they will very likely choose Avalara. I will keep an eye on the developments at the company and stay open-minded. What I hope to see in the next quarters and years is 1) control over the cost base and operating leverage as a result 2) continued growth in new customers/billings and Net Retention Rate and 3) a clear plan to realign management with shareholder value creation. I hope to see this before it gets snapped up by Private Equity.

Disclaimer: Always do your own research. This is not investment advice and for informational purposes only. Partnership Investing is not a registered investment adviser and may or may not hold securities discussed on this blog.