Industry analysis: Gaming and the Metaverse

An overview of the Gaming industry, its trends and an analysis of future developments. I will also discuss the Metaverse and how investors can think about it as an investment opportunity.

For my first industry analysis, I will discuss the Gaming industry and the Metaverse. I will try to map the industry and discuss my analysis of the industry, occasionally giving my sentiment on certain parts of the industry and where the industry might go. This will be a more Western-centric view of the industry, which might explain why you might find Tencent mentioned less often than expected despite them being the largest company in the space.

First, there are two books I used for this analysis and I would recommend to any investor:

Engines that Move Markets by Alasdair Nairn

One Up: Creativity, Competition, and the Global Business of Video Games by Joost Van Dreunen

The Metaverse has been discussed often by investors since Facebook changed its name to Meta. Zuckerberg has made clear that the development of the Metaverse will be one of his priorities in the next 5-10 years.

I’m very open to the idea and the opportunity the Metaverse might bring but do not pretend to know with any certainty how it might look if successfully developed. For investors excited about the Metaverse and exploring ways to invest in it, I will attempt to give my opinion on where in the value chain investors might find more success. This opinion is given with the limited information out there today and is mostly informed by my research on the commercialization of technological evolutions. By releasing this industry primer, which forms the basis of my view on the Gaming Industry and the Metaverse, I hope to spark engagement with other investors with similar interests and different views. Feel free to reach out through Twitter or the email address at the bottom of this post.

Let’s start with some key industry statistics:

Video Game market size is ~$180B according to Statista and Newzoo. Expected to reach >$250B by 2025.

Source: WePC.com, Statista, Newzoo

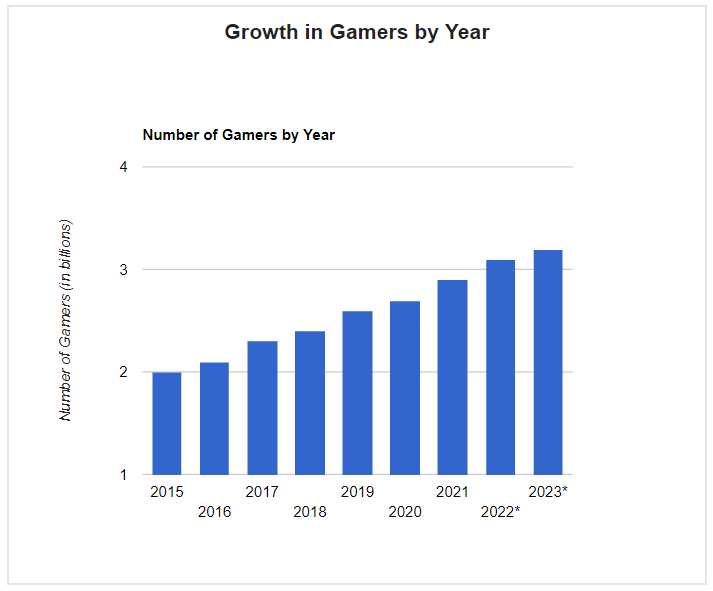

More than 2.9B gamers worldwide according to Newzoo.

Source: WePC.com, Newzoo

Mobile gaming was 52% of the industry, with consoles contributing 28% and PC gaming 20%.

Source: Newzoo

Asia-Pacific is by far the region with most gamers.

Source: WePC

Now that I have some context on the scale of the industry and high-level numbers, let’s give an overview of the entire value chain. To do this we will walk through the process of developing a game, publishing it, and distributing it on different platforms.

First, a game gets developed by a game studio. This studio is either an independent studio, a studio owned by a publisher, or a studio commissioned by a video game publisher. This stage in the value chain knows low barriers to entry. A studio essentially only requires talent and some capital to get started on a project. Modern tools like Unity and Unreal Engine provide developers the resources to create games of all sorts. On the larger projects, parts of the development project can even be outsourced to contractors like Keywords Studios.

The game is then published by a publisher or self-published as an indie game. This part is very similar to the movie industry with the major studios or even the music industry with labels. The publisher takes the responsibility of marketing the game and the distribution.

This is the part of the value chain that is most talked about. We will go deeper into this part when we go through the economics of video games.

Games can be distributed in various ways depending on the platform. Years ago, games were mainly distributed physically as CDs. These were the glory days of Gamestop as the largest retailer of video games. Nowadays, most games are distributed digitally. This shift to digital distribution has had large economic consequences for the industry (mainly positive, except for Gamestop).

Mobile games are mostly distributed through the Apple App Store and Google Play Store.

Console games are distributed digitally through the Playstation Store, Microsoft Store, and the Nintendo e-Shop.

The very first and wildly successful online games marketplace was Steam. Steam is a part of Valve, a business that also develops and publishes video games that was started by ex-Microsoft employees in the mid-90s. Twenty years after its launch. Steam still is the largest online games marketplace for PC despite efforts from other companies to build their own marketplaces. For example, PC games can be bought on different, mostly publisher-owned marketplaces like the Epic Store (Epic Games), Battle.net (Activision Blizzard), and the Origin Store (Electronic Arts).

The most successful distribution marketplaces, the App Store, Google Play Store, Playstation Store, and Microsoft Store are the result of these companies controlling the hardware or operating system (Apple with the iPhone, Sony with the Playstation console, Google with Android, and Microsoft Store with Xbox and Windows). Steam is a very successful marketplace for which the financials are unfortunately not available. It was one of the first to do this on PC and its network effects moat has endured until this day.

Some distributors, especially Apple and Valve, have been criticized for their anti-competitive tactics. Apple, for example, retains control over the iPhone/iOS ecosystem, and content providers, like Epic Games, and Spotify in non-gaming, have started to push back against the high App Store fees and the way Apple thwarts competition by making it impossible to make in-app purchases by bypassing the App Store.

The hardware manufacturers have gone through an interesting evolution. Playstation, Xbox, and Nintendo have dominated the console market for a number of years. They essentially sell the hardware at breakeven or relatively low margins to acquire an installed base of consoles. The advent of online/multiplayer gaming has solidified their lead even more as network effects started playing an even bigger role. Every new console cycle, which turns out to be every 7 years or so, these companies battle to increase the installed base. Playstation has been the most successful and has been in the lead since the Playstation 2 was released.

Source: Statista

The economics of video games

As discussed earlier, developing a video game has relatively low barriers to entry. A talented team of engineers and artists with capital and time to work could create an engaging video game. While this is true, the barriers to success in the video games industry are much higher. Like its Entertainment industry cousin, the movies industry, the video game industry is known to be very hit-driven. To maximize its chances of success, a video game requires a large marketing investment upfront to recoup the investment. Even with large marketing investments, commercial success is not assured. This has led video game publishers to find ways to minimize the effects of this hit-driven business or to increase the likelihood of success. There are a few ways the largest publishers have done this:

Consolidation: By consolidating the industry and becoming larger entities, video game publishers can spread their bets to decrease the risks and impact of commercial catastrophes. Acquiring, developing, and maintaining a portfolio of IP across multiple platforms has made these companies more stable and diversified. Look at the Activision / Blizzard merger, the recent Codemasters acquisition by EA or the most recent Zynga acquisition by Take-Two Interactive, or even the conglomerate Embracer Group as a whole, as prime examples of this strategy at play.

Licensing: By licensing known brands or names, game publishers increase their chances of success as the game already has a natural audience. The most successful examples are the FIFA and Madden sports franchises by EA, the Star Wars Battlefront games (again EA).

Franchise management: Once a game is a big commercial success, video game companies, much like Hollywood, try to make it a valuable franchise they can profit off from several years. A few of these franchises have endured and brought in billions of revenues a year. EA has its sports franchises and Battlefront, Activision Blizzard has Call of Duty and World of Warcraft, Take-Two Interactive has Red Dead Redemption, GTA and NBA 2K, Square Enix has Just Cause, Tomb Raider and Kingdom Hearts, Ubisoft has Assassin’s Creed and Far Cry. There are many others, some more niche than others. Having a franchise decreases the risks as players who liked the previous game(s) are likely to be receptive to the new release.

The possibility to deliver games digitally and the mobile phone have drastically changed the economics of the industry, how games are made and monetized. Traditionally, consumers would have to buy a copy upfront at full price. This was a way for publishers to recoup their investment immediately. With digital distribution and the low marginal costs of distribution it entails, games are now often free-to-play. In fact, according to Gamesindustry.biz, 78% of gaming revenues are from free-to-play games.

Gross margins for Take-Two, Activision Blizzard, Electronic Arts, and, Nintendo over the last decade.

Besides the economic advantages of digital distribution, the rise of mobile gaming has been largely through the free-to-play or freemium model. This makes sense, while there are tens of millions of consoles around the world, there are BILLIONS of people with a mobile phone in their pocket. This has led to widespread adoption of gaming beyond the traditional 18-34 years old male demographic. Gaming is now mainstream, with people from all walks of life gaming on their mobile phones during breaks, commutes or simply to pass time at home.

The strategy to make the game free so that it can reach as many gamers as possible to monetize them later on through in-game purchases or advertising makes a lot of sense and has had success for Zynga (now part of Take-Two Interactive), Supercell (majority-owned by Tencent), and King Digital (now part of Activision Blizzard). The free-to-play business model has now also taken over console gaming with games like Fortnite, Apex Legends, Overwatch, and Call of Duty: Warzone. The PC gaming world also has had major successes with free-to-play. League of Legends, Dota 2, and Minecraft are examples of games with incredibly large player bases, especially in Asia. In mobile gaming, Candy Crush, Clash of Clans, and Angry Birds are names that should sound familiar to most.

With new ways to monetize games arise new ways to build games. With the ability to better monitor player behavior, spending patterns, and gameplay, the creators of these games have a tighter feedback loop between the product they put out and how players interact with it. This enables the makers to quickly capitalize on trends to improve monetization by releasing new content at near-zero marginal costs. I would recommend you to take a look at the Q2 Quarterly Update to read how I think about feedback loops and the Decision Cycle.

Additionally, the incentive is now to keep the game fresh and enjoyable to retain the player as long as possible, increasing the lifetime value of the customer. Fortnite and Roblox have been two companies that have done a great job at creating hype to increase network effects. They have managed to create a lot of buzz and interest with special events, like Disney promoting their new Star Wars movie, Travis Scott, and Lil Nas X doing concerts. Electronic Arts and Take-Two Interactive have had a lot of success monetizing their sports games beyond selling the game copy. Ultimate Team (online play mode in Madden and FIFA games) generates about a billion $ in revenue and GTA V still generates hundreds of millions of high-margin revenue almost 10 years after its (record) original release. Talk about extending shelf life!

As you can probably make out from this, games have become more and more social experiences with very strong network effects at play. This trend has birthed companies like Discord and Twitch that do not produce any games but play an increasingly important role in the video gaming ecosystem. It has even led to a new form of sports, eSports. The global and social nature of games has resulted in some eSports events having more viewers than premiere traditional sporting events.

As we look to the future, a few new monetization models might evolve from what we currently see. With an audience of 47.3m Daily Active Users as of September 2021, Roblox has a tremendously large and engaged audience. This can also be said about Fortnite, which boasts 80m Monthly Active Users in 2020 according to leaked internal Epic Games documents. These types of audiences can be very valuable to advertisers and there will definitely be more advertising as a means of generating revenue. Advertising is already a large revenue stream for mobile games and I expect more of the same for games that can attract large, engaged, and valuable audiences.

Subscription models have not made any great breakthrough as of yet, but the attempts indicate that the large players are thinking about this. Microsoft has launched its GamePass and it already has about 25m subscribers. Publishers have also launched their own subscription services in an attempt to keep a larger part of the economics for themselves.

Google launched Stadia in 2019, a cloud-gaming service. This service, although very promising conceptually, was a failure and was scaled back in 2021. Playstation Now, Xbox Cloud Gaming, Nvidia’s GeForce Now, and Amazon’s Luna are other attempts to establish cloud-gaming services. If these services or another cloud-gaming service were to become successful, this could change the economics of the gaming industry. Instead of requiring every gamer to have a console, PC, or mobile with the specs to be able to run large, complicated games, cloud gaming runs the games in the cloud and streams tto the device of your choice. This changes the economic dynamic completely. Just like the installed base of mobile phones was much larger than consoles, now, even people with the most rudimentary hardware can experience large and complex games as long as they have an internet connection. This makes video games even more accessible, especially as you eliminate the lower upfront cost of buying a good PC or gaming console and exchange this for a subscription service.

Microsoft’s pending acquisition of Activision Blizzard is, in my estimation, an attempt to acquire high-quality content to attract players to the Xbox GamePass and Cloud offerings. This is a very strategic move and as we know from other types of media, content is king. Combining the distribution power Microsoft has through Windows / Xbox with the franchises Activision Blizzard has in their portfolio will drive significant improvements in the offering and attract many gamers to the service. Microsoft has a clear lead in this new category and they have been patiently building an impressive offering that boasts more than 25m subscribers already. With the Activision Blizzard acquisition closing in the next year or so, this 25m figure might be dwarfed by the influx of new players as they integrate Zenimax and Activision Blizzard IP in the GamePass offering,

Just imagine a subscription product that boasts multiples of this amount of subscribers in 5-10 years. The economics of this are bound to be drastically different than it is today and this could lead to a shift in the power dynamics between content and distribution.

Netflix and Apple have even started efforts to break into the gaming space. Apple Arcade has had limited success and Netflix has just recently announced its intentions. Using gaming to enhance other parts of the ecosystem is not a new thing. The Steam marketplace got traction by being a mandatory download to play Valve games and Epic Games is using the same tactic to grow its own marketplace. But it is the first time that large companies might enter the gaming space to enhance their ecosystem outside of gaming. Amazon, which is not known to be a gaming company, also has such efforts with Luna and Twitch. It is still unclear how gaming will fit in the ecosystem and strategy of tech giants.

To summarize, companies that have consolidated the industry have been rewarded handsomely by reducing the risks in their business. Digital distribution has revolutionized the way games are played, created, and monetized. The user bases nowadays reach tens of millions of people for large games and gaming has become increasingly social. Entire companies have sprung out of this social gaming ecosystem and I expect the gaming industry to continue to capitalize on these network effects. Distributors will keep trying to retain and expand control over their own ecosystem. It will be interesting to see how the dynamics between content and distribution will turn out in future years in the video game industry as monetizing methods and platforms change.

VR/AR

Virtual Reality and Augmented Reality are the latest evolution in interactive entertainment. The Meta Quest 2 (formerly Oculus) and the Playstation VR headset have been the most successful consumer VR headsets with millions of units sold each. It is estimated that around 12.5m VR headsets have been sold in 2021.

While the content is still limited for gamers that want to enjoy VR, the pieces are in place for it to become a burgeoning gaming platform. Developers are increasingly interested in the space, Unity and Epic are building the tools for developers to create content, and VR headsets have achieved a price point where millions of consumers are able to afford it. According to Omdia Research, VR content revenue was a mere $2B in 2021. This is a rounding error in the total gaming market, but the investments Meta and competitors are set to make in the next decade should grow this pie to become significantly larger. The expectations are high for VR and many are skeptical of how much consumer interest there will be in the end due to the natural limitations (VR requires space to move in, total immersion makes it difficult to engage multiple hours at a time). For a more mainstream consumer adoption, VR will have to offer content that is at least similar in quality than more traditional gaming platforms. We are still quite far off but VR/AR might be what bridges the gap betweenl gaming and the Metaverse.

Microsoft’s HoloLens 2 is more expensive and targets enterprises in need of VR capability. ASML, the Dutch semiconductor equipment giant, explained how the HoloLens 2 has made virtual inspection and consultation possible during the COVID-19 pandemic. This is a neat example of how VR can be used in the industrial world to help companies inspect plants and factories from distance. Other companies have been focused on the B2B possibilities VR/AR offers. Matterport offers services and software to create and navigate in digital twins. Real estate agents have used this for virtual sightings during the pandemic and many real estate marketplaces are pushing to offer this functionality on as many listings as possible. Unity announced a partnership with Hyundai to create a digital twin of a factory. This is not the first partnership of this sort and, as time goes on, I expect many more companies to explore how 3D environments and copies can improve their operations.

While most focus on the consumer applications of VR/AR, I find the industrial and B2B applications far more interesting. The B2B space traditionally has had higher switching costs. Consumer interest is notoriously fickle requires a lot of marketing spending to take off. Without network effects, a hit game or application can easily disappear. But a B2B application, where reliability, trust, and switching costs, rather than price, are carefully considered has much more chance of sticking around. It requires more investment into sales early on but provides more predictable cash flows over the long term.

We are still in the infancy phase of VR/AR, but I find it conceivable that this technology will find its way into business workflows and consumers’ households in the next decade or two. The key question is whether the companies providing this technology will be able to capture the value it creates. This is the billions dollar question with each technological innovation and one we will explore again for the Metaverse.

The Metaverse

The Metaverse is a term I first encountered through an Invest Like the Best podcast episode featuring Matthew Ball. Matthew Ball has many fascinating insights about the Media and Entertainment space and has been one of the most public voices about the vision of a Metaverse. It is probably best to let Matthew Ball’s words describe what the Metaverse is:

“The Metaverse is a massively scaled and interoperable network of real-time rendered 3D virtual worlds which can be experienced synchronously and persistently by an effectively unlimited number of users with an individual sense of presence, and with continuity of data, such as identity, history, entitlements, objects, communications, and payments.”

Fortnite, Roblox, Minecraft, and some other 3D worlds have been described as “Metaverses”, but this description is much like saying Google and Facebook are their own Internets. These can be better described as experiences within a larger Metaverse. Changes to this Metaverse will be permanent and an unlimited amount of people can in the same experience at the same time. This vision promises the emergence of a thriving digital economy where people can earn money, exchange goods and deliver services to participants. This will be done at an even larger scale than the games mentioned before and will have some overlap between our digital and physical lives. The potential to create an entirely new digital economy through connected, immersive, and interactive entertainment is something we can be excited about. The Metaverse draws inspiration from books like Snowcrash and Ready Player One. Ironically, these books actually describe a dystopian world, much like how the telescreens are used to spy on citizens in Orwell’s 1984 and the way people are enslaved by technology in Huxley’s Brave New World.

The Metaverse has been introduced to the mainstream by Facebook changing its name to Meta Platforms after the announcement that they would focus on building the next platform for the Metaverse. While this might seem like a sudden shift of attention and the $10B a year investment raises some eyebrows in the investment community, I think this has been carefully thought out by Mark Zuckerberg. Internal emails going back to 2016 show that Zuckerberg was arguing to acquire Unity Software, now a publicly-traded company, to gain control over the next platform. Facebook now is under more scrutiny than ever in an antitrust context, Zuckerberg is conscious that if the Metaverse is the next platform, Facebook cannot acquire its way into it as it did with Instagram or WhatsApp when Facebook needed more mobile presence and that not being an important part of this new platform would put Facebook in jeopardy. Seeing how well Apple, Google, and Microsoft have done by having control of their platforms, Zuckerberg sees the successor of the Internet as an opportunity to put his company in the driver’s seat instead of being at the mercy of his Silicon Valley counterparts.

The vision of the Metaverse is there and the Metaverse is coming. Companies beyond Facebook, which I will now refer to as Meta, have embraced the idea of contributing to building the Metaverse. Epic Games, Nvidia, Unity Software, Roblox, and even Microsoft have used the term and seem to have it as an important part of their future ambitions.

Now that the basics of the Metaverse are covered and what it promises, I will go into how I think about investing in the Metaverse.

Investing in the Metaverse

There is probably nothing more exciting for an investor to invest in than companies that are on the bleeding edge of technology and innovation. The potential seems unlimited and even a moderate position in the promised end-state of the innovation would result in big financial gains for early investors. The truth is often much different.

After studying technological innovations and how it interacts with the financial markets, I can’t help but be careful about investing in technological innovations with a lot of hype around it. In his amazing book Engines that Move Markets, Alisdair Nairn gives a few patterns to recognize a bubble:

- Emergence of new and potentially transformative technology about which extravagant claims could be made.

- Climate of relatively easy money and credit conditions

- General investor and consumer optimism

- A wave of new publications promoting the merits of the technology

- Efficient supply machine capable of creating companies to meet investor demand

- Suspension of normal valuation criteria

I would argue that the Metaverse checks all boxes and this is a good reason to be cautious.

Additionally, the promise of the Metaverse being an open ecosystem much like the Internet raises a few questions when we look at the historic development of the Internet. The interoperability and openness of data needed to deliver on the promises are in stark contrast with how the most successful Internet companies have captured value in the last 20 years. Much like other technological innovations, the Internet created a lot of value. But most of this value did not accrue to individual companies but to consumers. To capture a part of the value created, successful Internet companies have built so-called “walled gardens” where data from within these walled gardens was rarely shared outside of its walls. Building the Metaverse technologists and consumers hope for will require a large amount of cooperation and coordination between companies with sometimes different interests.

Path dependence can play a key role in how technologies evolved and get adopted. This reduces one’s ability to predict the end-state of the technology and how it is used. Disruptive technologies force us to change habits, learn new things, and redefine laws. This sometimes leads to what economist Brian Arthur calls “lock-in”, where markets and economies get “locked” in a suboptimal state. The most famous example, though still questioned, is how we settled on the QWERTY keyboard instead of more efficient keyboard layouts.

Without even mentioning the technical aspects needed to enable the Metaverse and how unpredictable those developments will be, just imagine how the concept of legal ownership needs to be redefined by legal systems around the world for the Metaverse to become what its most enthusiastic proponents hope. How would it work if your rich uncle passes away and you inherit his digital goods and NFTs? How would your wife be able to claim 50% of your digital avatar collection after she dumps you because you spent all your time in the Metaverse?

Some of these questions might be easy to answers, others will definitely not be. And with governments and lawmakers still wrestling with questions on how to regulate Internet platforms, I wouldn’t count on them to be both quick and effective in drafting legislation to accommodate this new reality.

I could stop here and say: “Don’t invest in the Metaverse, it probably is a bubble and recognizing the winner is extremely difficult”. But that would be no fun nor intellectually stimulating. Despite some healthy skepticism and doubt that I am smart enough to predict the outcomes that will matter, I find the idea of the Metaverse very intriguing. I see how it could be the natural evolution of how the Internet, gaming, and social interaction have developed in the last decades.

Using the history of investing in technological innovation, is there a way we could identify the companies or areas of the value chain that might do well? I think there is, though I try to stay humble in my assessment. Technology can move very fast and winners, as well as losers, can emerge in a short window of time, at any point between infancy and maturity. If anything, it is an interesting thought experiment that might direct you to some interesting ideas.

First, we should look at companies that are not solely reliant on the benevolence of the capital markets. Companies that have strong balance sheets and/or can self-fund their growth simply have a higher chance to make it to the finish line. This is not a very novel concept, but often gets forgotten by investors caught in the excitement.

Second, companies that have a competitive advantage can defend their returns from competitors that enter the space. While in the past, this was mostly done through patents or government-enabled monopolies (Western Union, AT&T, General Electric, RCA), I suspect this will be done mostly through controlling your ecosystem, network effects, and scale advantages in the Metaverse era. This is much like Microsoft, Apple, and Google in the PC and later the Internet era. PC hardware manufacturing or building single applications were not as good businesses as controlling the platforms. This is why I believe that companies like Epic Games, Roblox, and, possibly Meta have an early advantage. They have experience with controlling and growing their ecosystem through network effects and have the financial strength to keep investing.

Third, the well-known “picks and shovels”. While capital and resources are being invested - perhaps wasted - for the promises of insane riches, companies supplying the tools to realize those dreams can benefit more than the direct winners. Within the context of the Metaverse, we might go as far as looking at the cloud computing providers, networking infrastructure players, or even semiconductor manufacturers who could make the Metaverse possible. This would be quite a stretch in my opinion. Surely, these companies would benefit, but it is currently still undefined what chips will enable rendering the Metaverse or what the networking infrastructure will look like.

To us, the more obvious players to look at are the companies that enable the production of content for the Metaverse, which is a sine qua non for widespread adoption. Without engaging content, there is no Metaverse nor any demand for it. Unity Software and Epic Games (with the Unreal Engine) have built tools that enable creators to build engaging and immersive 3D worlds. There is a good chance the tools used to build the Metaverse will not be too dissimilar and that these two companies will play an important part. The network effects to become an industry standard and scale advantages these two game engines have will be difficult, though not impossible, to displace for any competitor entering. For the Metaverse to be a success, a large variety of experiences will need to be available and it is hard to see each developer building their own engines to build them.

Unity’s acquisition of Weta Digital, the technology part of WetaFX, and the use of the Unreal Engine for movies and TV. WetaFX worked on many blockbuster names any movie-goer would recognize. The tools they have built to create the VFX in movies like Avengers, Lord of the Rings, The Hobbit and, Avatar are now in the hands of Unity. For the first time, creators outside of WetaFX will be able to use those tools to create their own worlds and experiences. This opens up a tremendous amount of possibilities for creators both in films and gaming. Epic’s Unreal Engine 5 was used in the hit shows The Mandalorian, Westworld, and in Ford vs Ferrari. For anyone who has not had the chance to watch some of these, the quality of the VFX is incredible. Seeing these tools at work in movies, TV shows and interactive entertainment offers an exciting perspective on how the technology can be used to make the creator’s vision a reality in different formats.

Lastly, there are some types of businesses or areas of the Metaverse it is too early to tell the structure but will enable commerce. Think about payment solutions, marketplaces, advertising, and digital goods. We have some references to how it might look, but it is very unwise to count on any outcome. PayPal or Square might dominate the payment space in the Metaverse and OpenSea could become the premier marketplace for NFTs and other digital goods, but would you prefer to bet on it now or when there is a clearer path to getting there?

Companies that can enable commerce and essentially function as a royalty on the Metaverse GDP can and will surely become very profitable through ecosystem control, network effects, and scale advantages, but it is too early to have any conviction on the end-state.

Realizing that these outcomes often follow a Power Law might give investors pause before betting on a horse. Out of the top 10 largest companies in the S&P 500 at the beginning of 2022, 3 of them were not public 20 years ago (Alphabet, Meta, Tesla), 2 were not even founded (Tesla and Meta) and the modern-day giant Apple had a mere $5B market cap. If we go back 25 years, Alphabet wasn’t even founded yet, Nvidia was not public, Apple had to be saved by Microsoft, and Amazon just went public. This is both the beauty of technological innovation and its challenge. Companies can rise or die fast, but great success is only for a (lucky, privileged, or deserving?) few.

To conclude my views on investing in the Metaverse, I would recommend any investor to study past technological innovations, their adoption curves, and the patterns to identify winners. I have found this to be a very humbling experience and it has somewhat tempered my confidence about investing in the Metaverse. Recontextualizing the present vision of the future - which feels novel, exciting, and optimistic - to the past makes us realize that these novel ideas are just more of the same; technological progress. Investors in the 1840s probably felt the same about railways as people do now about the Metaverse. The same could be said about many periods that produced world-changing technological innovation, yet there are probably more investors and companies that lost out than those that were successful.

Recommended resources:

Engines that Move Markets by Alasdair Nairn

One Up: Creativity, Competition, and the Global Business of Video Games by Joost Van Dreunen

Matthew Ball blog

Disclaimer: Always do your own research. This is not investment advice and for informational purposes only. Partnership Investing is not a registered investment adviser and may or may not hold securities discussed on this blog.