Unit Economics

Our thoughts about an alternative business analysis method

Financials of companies are mostly analyzed on an aggregated basis. Most companies report their aggregated income and these figures are widely displayed. However, aggregated income may give a distorted picture of the economics of a business. In this article, we will introduce unit economics, show its importance and put unit economic analysis into practice.

By looking at the unit economics, one analyzes the added value per unit. A company can earn negative earnings in total, but be profitable over a lifetime as a unit generates revenue and profits. Companies have to invest a lot to acquire customers at the start of a business. This could create negative earnings or even negative cash flows. However, this is at the beginning stage and could include one-offs such as one-time capital expenditures. One should look at the lifetime value of a unit instead of the aggregate results at a specific point in time. For example, Amazon had negative earnings for years before showing profits. On a unit (per customer in this case) basis, Amazon made an operational profit but it reinvested every dollar back in its business, creating a loss on an aggregate basis.

Imagine, a company has to spend 300 dollar per unit upfront to start its business (spent on capital expenditures, inventory, etc.). A unit would generate 100 dollar of revenue per year. Including costs to maintain the unit of 20 dollar per year, the results would look terrible in the first years. However, the starting costs will be paid back in 3 to 4 years. If a unit generates revenue for 10 years, then the results per unit will be tremendous. We can use this method to identify early-stage growth companies that are likely to be very profitable at maturity. Venture capitalists often use this to measure the performance and potential of companies.

This could be true for traditional business models such as retailers with physical stores as well as new businesses with online shops. In the beginning, retailers have to build or rent a store and invest capital in interiors and inventory, causing negative earnings. However, if the retailer has high enough margins per sold product for a long enough time, then the profits could transcend the initial costs. The same logic applies to online businesses. Online businesses first have to invest capital in their website, logistics, and the acquisition of customers. If their customers add enough value over their lifetime, profits will transcend the initial and structural acquisition costs.

Analyzing unit economics is used more as business analysis than financial analysis. It is a tool to understand the economics of a business. With unit economics, one could estimate the contribution margin per unit or how many units and time are needed to break even. With the analysis one also takes into account the analysis of competitive advantages. The lifetime value of a unit takes into account the duration a company generates revenue, the costs the company has to make to acquire and maintain the unit, and the profits the company makes over the units’ lifetime. To forecast the profits, one has to analyze whether the same prices are maintainable. Does the company have enough added value for clients to maintain the customer? Do they have pricing power?

It also says something about the capital allocation skills of management. Is management aiming to add more value per unit or to grow the number of units?

How to determine the unit?

One should first start with identifying the unit. The nature of the business determines the units. A unit could be a customer or a store. It depends on what the ultimate revenue driver is. Who is the unit and what is the income per unit? In this regard, a unit could be a client as we have seen in the Amazon example. However, a unit could also be one store. How much capital is needed to set up a store and what is the payback time?

After we have identified the unit. We are going to analyze the economics of the unit. In this analysis is the cost to acquire, produce, recruit or service a unit and the revenue a company generates in the lifetime of a unit. Together is called the lifetime value of the unit.

The lifetime value of a unit

Now, let's take a look at the elements of a unit economic analysis. To calculate the lifetime value of one unit we use the following formula:

Gross profits per unit is the revenue per unit per period minus its costs of goods sold during the same period. In this case one analyzes the revenue per unit, subtracting revenue derived from non-operating sources such as one-time events and non-recurring revenue. The magnitude and durability of gross profits depend on the durability of its competitive advantages. The more competitive advantages a company has, the more it can raise its prices and thereby gross profits. Conversely, stable and increasing gross profits could indicate a widening moat.

x is the units’ lifetime. It is the duration a unit is generating revenue for the company. The lifetime can be measured by taking the inverse of the churn per period. Churn is important in multiple ways; a lower churn will make a unit add more value if it generates positive cash flows and the company has to invest less per unit to generate the same cash flow. Both increase the lifetime value of a unit. Churn is influenced by multiple factors; customers will stay longer when they are satisfied, when there are switching costs and when they are socially connected.

The WACC is the weighted average cost of capital. Future cash flows should be discounted by the WACC to take into account the time value of the cash flows.

Costs are the costs to support the service of clients and operations of the business during a specific period. These costs include operational expenditure, R&D, etc.

CAC, customer acquisition costs, are the costs incurred by the company to acquire a customer or in the case of physical retailers the costs incurred when opening a new store. The CAC is incurred once per acquired unit. A company might be able to lower CAC when it enjoys network effects. The higher the network effects of a company are, the higher the power of its services/products, and the more people are inclined to join the network. If the network is powerful enough, a company attracts people without spending on marketing or sales.

Trade-offs

The above elements together form the lifetime value of a unit. Forming the lifetime value, the underlying elements interact with each other and there are trade-offs among them. For instance, a price increase raises gross profits but could increase the churn rate as well. The same goes the other way. The churn rate decreases as the price decreases, but then gross profits also decrease. A company could lower churn but that would increase retention costs. Targeting new customers increases customers but raises acquisition costs. A company should bear the trade-offs in mind when thinking about its capital allocation strategy.

Unit economics analysis: Atlassian

Now that we know the background of unit economics, we take it into practice. In this part of the article, we try to show the importance and application of unit economics in the investment analysis process.

Since companies do not disclose all the necessary figures it is sometimes hard to come up with unit economics. However, we try to illustrate the power of unit economics analysis with a dive into the financials of Atlassian (ticker: TEAM).

Atlassian delivers SaaS collaboration and development solutions. It has products such as Jira and Trello.

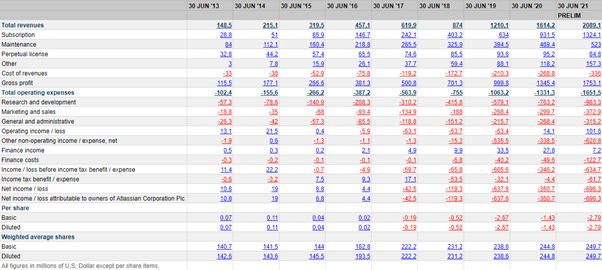

Below you can find the income statement of the company from the past years:

(Source: Factset)

As you can see, the company had a net loss in the past 5 years. They even had operational losses in several years.

Still, the company is almost a 15-bagger since its IPO in 2015. So, the company should create some value, one would say. Analyzing the unit economics we come up with the following results:

(Source: own estimates)

We look at the economics per customer level to analyze the unit economics. We calculate the revenue per customer by dividing the total revenue by its number of customers. We use the top-down method to come up with the revenue per customer to obtain more in-depth information about the revenue per customer data over the years.

Usually, one estimates the average revenue per unit with a bottom-up approach to use the analysis for future estimations. However, we do not have all the necessary information about Atlassian and we do not think it is within the scope of this article. We use this case to exemplify the importance and essence of unit economic analysis.

We subtract the cost of revenues and operating expenses such as General and Administrative, obtaining the operating profit. Atlassian uses its R&D for improving and adding products to acquire but also to keep customers. Atlassian did not disclose how much they use to acquire customers, so for convenience, we include R&D in the unit economic analysis. The company did not pay taxes in most of these years since they did not make a profit on an aggregate level. However, on a unit level, they did make a profit, so we use the standard tax rate. We multiply the operating profit after taxes with the lifetime of a customer (the inverse of churn, assuming that churn is stable at 2% over the years) and calculate the net present value. After subtracting the CAC we arrive at the Lifetime Value of an average Atlassian customer. The CAC has been calculated by dividing the sales and marketing costs expenses by the number of added customers.

The Lifetime value per customer has been positive in 4 of the last 7 years and is on average positive. The CAC presents a hefty part (around 80%) of the LTV of an Atlassian customer. The CAC is a one-time cost and is an investment to acquire a customer. Atlassian is still making a loss on an aggregate level. However, if Atlassian matures, keeps its CAC low, sustains its competitive advantages, customers will stick and the company could turn profitable.

LTV/CAC

A common ratio to look at when analyzing the unit economics of companies is the LTV/CAC ratio. In the ratio, the LTV is often defined as the average annual revenue per customer minus the direct costs to fill an order, times the retention time. A ratio above one implies that a company is adding value and vice versa. Generally, a ratio greater than 3.0 is regarded as good. The ratio can also be used to compare the value creation with competitors. According to the definition of LTV, in contrast to our previous LTV calculation, we should not include R&D. Not including R&D we arrive at 3.6 on average. So, although the company makes a loss on an aggregate level, it does perform well on a unit economic level according to the LTV/CAC ratio.

As you can see, we made a lot of assumptions about the unit economics of the company. Although some figures will not be totally accurate, making assumptions about unit economics is a good exercise to analyze a business.

Resources and recommended readings:

Bluegrass capital on Unit Economics: https://acquirersmultiple.com/2019/12/ep-40-the-acquirers-podcast-bluegrass-capital-unit-economics-incremental-returns-and-intangible-capital/

Elliot Turner on Unit Economics:

Michael Mauboussin on Unit Economics: https://www.morganstanley.com/im/publication/insights/articles/article_theeconomicsofcustomerbusinesses.pdf?1621441813718

Tren Griffin on Customer acquisition Costs: https://25iq.com/2016/12/09/why-is-customer-acquisition-cost-cac-like-a-belly-button/

LTV/CAC ratio: https://corporatefinanceinstitute.com/resources/knowledge/valuation/cac-ltv-ratio/

Disclaimer: Always do your own research. This is not investment advice and for informational purposes only. Partnership Investing is not a registered investment adviser and may or may not hold securities discussed on this blog.