Vitec Software (VIT.B-SS) - A Swedish compounding machine

We add Vitec Software to the Partnership Investing portfolio. This serial acquirer reminds us of a smaller Constellation Software with lots of room to grow.

Vitec Software is a Swedish software company founded in 1984 by Lars Stenlund and Olov Sandberg. The company’s growth strategy consists of buying niche VMS (Vertical Market Software) companies in the Nordic region. Vitec might be considered the Nordic equivalent to Constellation Software due to the similarity of their growth strategies and focus on VMS.

Investment case

Vitec Software is a company with a track record of successful M&A, having acquired more than 30 companies since starting their acquisition-driven strategy in 2003. Vitec’s businesses have mid-single-digit organic growth and require very little capital investment to grow organically. The founder and Chairman of the Board, Lars Stenlund, is still involved in the business and has proven himself a great industrialist. Under him, Vitec has grown into a company worth 10bn SEK (1bn euro, the SEK/EUR ratio is ~10 to 1) that has been a 30-bagger in the last 10 years. Vitec has been able to reinvest its cash flows into profitable acquisitions, yielding a cash ROIC of ~30%. We believe Vitec still has a lot of growth ahead and can keep reinvesting its cash flows at very attractive rates of return for the foreseeable future.

Business overview

Vitec Software consists of 29 different business units. These business units all serve niche vertical markets in the Nordic region. An example of a typical Vitec business would be a company that serves Finnish waste management companies and has about 50m SEK in revenue (this example was actually given when we spoke with the company). Vitec businesses serve all kinds of end-customers in many different verticals (real estate, healthcare, banking, just to name a few).

Source: Company presentation

These businesses do not face many competitors in their niche and are often number one, two, or three within their niche. Although they do not often lose customers, these VMS companies also do not have many growth opportunities left, most often growing in the mid-to-low single digits percentage points per year. In short, the subsidiaries are mini-monopolies or oligopolies.

The business units keep a lot of autonomy and strategic decisions are made by the employees of the business unit, not at the corporate level. Vitec believes the people closest to the customers are the ablest to make these kinds of decisions. The business units get the resources more common at larger companies (training, finance and HR infrastructure, etc.) while maintaining autonomy to keep the entrepreneurial culture intact. The business units are monitored using key metrics with a focus on cash flows and recurring revenues. This decentralization in the organizational structure reminds us of Constellation Software, although it is important to state that this decentralized structure seems more common in Scandinavian countries.

Vitec launched its acquisition-driven growth strategy in 2003. The company has had great success acquiring and integrating these VMS businesses. Revenues have grown from 492m SEK in 2014 to 1.3bn SEK in 2020, or a 17.8% CAGR. EBITA (Earnings before interest, taxes, and amortization) has grown from 92m SEK in 2014 to 345m SEK in 2020, a 26.5% CAGR. Cash flows have followed suit, Cash flow per share has grown from 4.40 SEK per share to 13.18 SEK per share. EBITA margins have expanded from 19% to 26% over the same period, a testament to the success Vitec has had acquiring and integrating new business units. Now that we know the results of their M&A strategy, we will take a deeper look at how they achieved such success.

Serial acquirer

Vitec has acquired more than 30 businesses over the years (some have merged). Over the last 8 years, Vitec has done between one and five acquisitions a year with deal sizes ranging between 20m-90m SEK. Vitec’s sweet spot is in the 30m-60m SEK deal size. Multiples paid for these acquisitions have been reasonable, mostly in the 1-2x EV/Sales and ~5x EBIT range post-synergies.

We believe that Vitec is often the buyer of choice for entrepreneurs who want to sell their business to a trustworthy partner. Like Constellation Software and Topicus, Vitec offers a good home to someone’s life work, the sellers most often being older entrepreneurs looking to retire or be less involved in the business. The culture at the acquired businesses is kept in place and growth opportunities are offered to employees. This makes Vitec more likely to be the preferred buyer and distinguishes them in a world with many financial buyers that will not offer the same continuity in the business or foreign acquirers. This reputation in the Nordic region is a source of competitive advantage when it comes to acquisitions as price becomes a secondary consideration to cultural fit, legacy preservation, and continuity for employees. With 20 years and more than 30 acquisitions under their belt, Vitec is well-recognized in the region. It would take other acquirers years to develop the reputation Vitec has in the Nordic VMS market.

The size of the businesses Vitec acquirers somewhat insulates Vitec from Private Equity competition. The competition from financial buyers, mainly PE, gets more intense as the businesses cross the 100m SEK in revenue threshold. Many of the Vitec targets are thus too small for these buyers. Our conversations with the company indicated that PE competition has not seemed to impact multiples or the appeal for entrepreneurs to sell to Vitec.

Additionally, the niche, saturated, and monopolistic/oligopolistic nature of the markets these businesses operate in make them less appealing to strategic buyers. This leaves aggregators like Vitec and financial buyers as possible acquirers, thus further reducing Vitec’s competition in the acquisition process.

Vitec still invests in the businesses after the acquisition, which has resulted in mid-single-digit organic growth in the last few years. Based on our calculations, Vitec has been able to generate a 30% ROIC on these acquisitions over the last eight to ten years. The ROIC is calculated as incremental EBITDA per SEK spent, an imperfect calculation method, but looking at long-term financials and acquisition multiples, 30% seems to be the right number. This is a great return and is the single most important driver of Vitec’s performance over the years.

Source: own estimates

Vitec has invested ~75% of their Free Cash Flow into acquisitions, distributing the rest in dividends. Considering Vitec’s M&A track record, distributing dividends seems like a sub-optimal way to allocate capital. We attribute this to the more dividend-oriented European investment culture. This is also probably a way for Lars Stenlund to create an income stream, considering most of his wealth is invested into Vitec shares and the modesty of his salary.

We see a long runway for growth for Vitec. The company still is 15-20% the size of Topicus, a Constellation Software spin-off that operates in Continental Europe. Vitec still sees about 500 companies fitting their acquisition criteria in the Nordics, with about 100 of them on an annual shortlist. Vitec does not actively pursue acquisitions on Continental Europe, preferring to focus on the market they know best, the Nordics. Expansion beyond the Nordics might be an opportunity they pursue in later years, but we do not factor this into our investment case.

Source: Company presentation

Topicus and Constellation Software acquire at a much faster pace than Vitec and spend a larger percentage of their Free Cash Flow on acquisitions, which explains the higher multiple at which Topicus is currently valued (we prefer to compare Vitec to Topicus for valuation as they are smaller and have a more or less similar growth runway). Additionally, CSU and the TSS part of Topicus generally have a lower organic growth profile than Vitec, hinting that Vitec invests more in their businesses.

Management and Ownership

Lars Stenlund, the co-founder and Chairman of the company, was until recently CEO. He has stepped into the Chairman role in 2021 and the CFO Olle Backman has stepped into the CEO role to replace him. Stenlund owns about 4.90% of the share capital but has 26% voting power through A-shares (the publicly listed shares are B-shares). His co-founder Olov Sandberg still has 3.64% of the share capital and 19% voting power through A-shares. The CIO/CTO, Jerker Vallbo, owns 1.35% of the company and has 6% voting power. The company also counts other individuals on its cap table along with long-term oriented investors like Capital Group and Spiltan Fonder. As of the Annual Report 2020, Olle Backman, the new CEO, did not own a significant amount of shares. Although he joined the company in 2019, this is something we would like to see change in the next few months as he gets further into his CEO role.

We see this amount of insider ownership and control as a good sign. Management talks a lot about how they think long-term and we think this structure allows for them to execute on their vision. The control aspect is obviously something we only like when the people in charge have a good track record, which Stenlund has.

Remuneration is quite straightforward. Senior management is paid a cash salary and can participate in an incentive program. The salary portion is not extravagant, the CEO receives 2.5m SEK (or 250K euro) and the other 3 members of management collectively receive 5.8 SEK (580K euro). After Stenlund’s departure as CEO (he is now Chairman), we wouldn’t be surprised if the new CEO, Backman, receives a higher salary than Stendlund received as CEO.

The incentive program is simply a grant of warrants that expire 3-year after the grant date (2023 for the 2020 issue). The 2020 incentive program granted warrants with a 333 SEK exercise price and the 2021 issue has an exercise price of 463 SEK a share. Participants paid 50% of the premium for these warrants. Participants will only reap the rewards if the Vitec shares are worth more than 463 SEK in 2024 (excluding the paid premium), this is equal to an 8% annual growth in share price. We view this incentive structure as very conducive to a mindset of long-term shareholder creation.

Financials and valuation

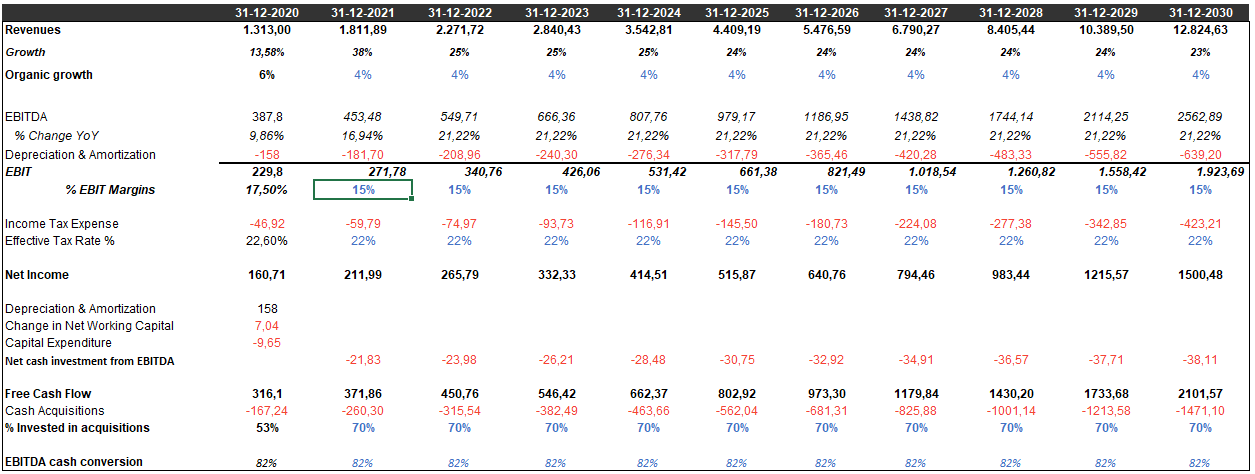

Vitec generated 1.31bn SEK and 1.16bn SEK in 2020 and 2019 respectively. This represents a 13.5% growth rate, of which 6% was organic. Organic growth has been stronger in the last few years. We think the 4-6% level is a realistic assumption for future organic growth.

Vitec measures its profitability with the EBITA metric. This adds back the amortization due to past acquisitions and assumes capital expenditures are similar to the expensed depreciation to make it a good proxy for pre-tax FCF. EBITA was 345m and 247m in 2020 and 2019 respectively, or a 26% and 21% EBITA margin. This metric has historically approximated FCF, but we will use assumptions about cash conversion of EBITDA to calculate our projected cash flows. As Vitec’s business gets more and more recurring revenues, cash conversion should be quite high (80+%).

Vitec’s growth strategy is centered around acquisitions, it is important to have some idea of how much cash Vitec will spend on acquisitions and how much cash returns they can expect on their investments. We have taken a look back at past acquisitions and approximate that Vitec has generated around 30% cash returns on their acquisitions. Vitec’s FCF deployment into acquisitions has been lumpier and it is difficult to predict exactly the amount and timing of these acquisitions. Based on historical results we expect Vitec to deploy on average ~70% of their FCF into acquisitions over the next few years. This might be higher as only 16% of FCF is distributed as dividends at the moment. In fact, we hope Vitec deploys even more FCF than this 70% assumption as long as they can achieve good returns on invested capital.

Tying all this together, we arrive at the following key assumptions:

Organic growth: 4%

Pre-tax Return on Invested Capital (calculated as incremental EBITDA per SEK spent): 30%

EBITDA to FCF conversion: 82%

Percentage of FCF spent on acquisitions: 70%

For this model, the revenue projections are irrelevant. The key inputs for the income statement are centered around 1) organic growth (assuming 4% organic growth equals 4% in EBITDA growth) and 2) incremental EBITDA on acquisition spend.

Source: own estimates

This is how the M&A projections would look beneath the surface.

Source: own estimates

Using these assumptions, we can estimate Vitec Software’s value with a DCF and Exit Multiple Valuation.

Using a 10% discount rate and 2% terminal growth rate, Vitec would be worth around 499 SEK a share according to our DCF. This would imply a 22% discount to the current share price of 390 SEK.

Using the Exit Multiple Valuation method, Vitec would also be worth much more than current market prices. Our FCF estimate of 2026 is 971m SEK. At a 25x multiple, this would get Vitec to a 24.3Bn SEK market cap. Assuming 3% dilution, this would imply the Vitec shares would be worth 715 SEK per share in 2026, or a 13% IRR over the next 5 years.

We find these assumptions reasonable and on the conservative side. We would not be surprised if Vitec could outperform these expectations by 1) improving profitability, 2) acquire at a faster pace, 3) improve organic growth to 5-6% a year, or 4) have higher returns on acquisitions. These are the four main levers Vitec could pull to compound at an even faster pace.

Conclusion

Vitec’s current valuation seems quite expensive. But as you can see, when a company can compound FCF per share at a fast pace, the current P/E or EV/EBITDA ratio can be deceptive and make you overlook a high-quality compounder solely due to the high multiples. This way of looking deeper than the traditional valuation metrics is a trend that you might have noticed from our previous articles. Some companies might not even look profitable, like Naked Wines or Intellicheck. Some might be profitable but look expensive. It is our job as analysts and investors to look under the hood and figure out how profitable the company truly is and can become.

A risk to our investment thesis would be that Vitec does not deploy nearly as much of its cash flows as we expect and/or the returns on their acquisition are materially lower than historically. This could come from higher PE competition as Vitec acquires larger businesses, driving down returns on investment. This risk is mitigated by the relatively small-sized acquisition Vitec targets and the number of companies they could still acquire. This provides Vitec with more opportunities to reinvest their FCF for a long period of time.

Degradation on a business unit level is also a risk. The business units need to keep adding value to their customers. We trust management that with their experience in VMS they will keep the business units agile and find, develop and retain talented managers for the business units. We trust that Vitec management is good at what they do, acquiring and managing software business. Vitec’s organic growth history gives us confidence that their model works and they can manage those businesses well into the future.

We think Vitec’s shares will be worth significantly more in a few years. With a talented capital allocator and industrialist at the helm, proven company culture, and plenty of room for growth, we think our capital will compound nicely by buying Vitec shares at the current market price. We would, however, wait for a pullback to build a large position in Vitec shares. The quality of the business is still better recognized than Naked Wines or Intellicheck, which translates to a higher valuation. A 20-30% decline in price would provide the opportunity to add to our position in Vitec that could compound at >20% a year for the next few years.

We would like to finish by inviting any reader to reach out and recommend or talk about your favorite Nordic stocks. We have found a good amount of quality companies in these markets we would like to look further into. Feel free to DM us on Twitter @PartnershipInv or email us at partnershipinvestingblog@gmail.com.

Disclaimer: Always do your own research. This is not investment advice and for informational purposes only. Partnership Investing is not a registered investment adviser and may or may not hold securities discussed on this blog.

Excellent write up. Any idea why they issued equity in late 2022?

Vitec spends around 10% of their revenue on maintain capex, which could be good to know.

i think it might be hard to keep the growth rate over time since its just a number of these busnisses that will be up for sale each year. 1-5 historically as you mention. Maybe need to go into Europe to increase aquicition frequency?

Another similar company is CSAM Health in Norway, they specialice in e-health though and are at an even earlier stage ~350mNOK in rev. Higher organic growth and margins though, and also cheaper. Maybe thats the way you disrups CSU and Vitec, by consentrating on one nische to become the prefered buyer?

Could also recommend looking into Protector Forsikring, like Geico they grow from being the most efficient insurer with huge cost benefits over peers. Long runway and great leaders. Last but not least, a bargin due to some bad luck last years and damage inflation that they underestimated at first but have sorted out now with huge price increases.

/S&U